This playbook is designed for operations leaders, digital transformation teams, and technology decision-makers in Banking, Financial Services, and Insurance (BFSI) who are evaluating, or actively implementing, AI-powered dispute resolution.

Dispute management sits at a critical intersection: it directly shapes customer trust, consumes significant operational resources, and carries real regulatory weight. Yet most institutions still handle it through fragmented, manual, or semi-automated processes that were built for a world where digital payments were a fraction of today’s volume.

This guide draws from industry research by McKinsey, Salesforce, Forrester, and AWS, as well as Lyzr’s direct implementation experience with BFSI institutions. It provides practical frameworks, not just concepts, to help you move from assessment to production quickly and responsibly.

What’s Inside:

- The $3B dispute crisis, and what’s driving it

- A 4-stage automation maturity model for BFSI

- Step-by-step agent architecture for each dispute lifecycle stage

- Human-AI collaboration framework and decision boundaries

- Zero-trust governance model: RBAC, kill switches, audit trails

- 4-week implementation roadmap with week-by-week milestones

- KPI tracking framework and ROI benchmarks

- Readiness checklists and action planning worksheets

How to Use This Guide

Each chapter builds on the last, but they can be read independently based on your current priority:

- If you are framing the business case → focus on Chapters 1, 2, and 11

- If you are designing the architecture → focus on Chapters 5, 6, 7, and 8

- If you are planning the rollout → focus on Chapters 9 and 10

- If you need to build a governance framework → focus on Chapters 8 and 9

Executive Summary

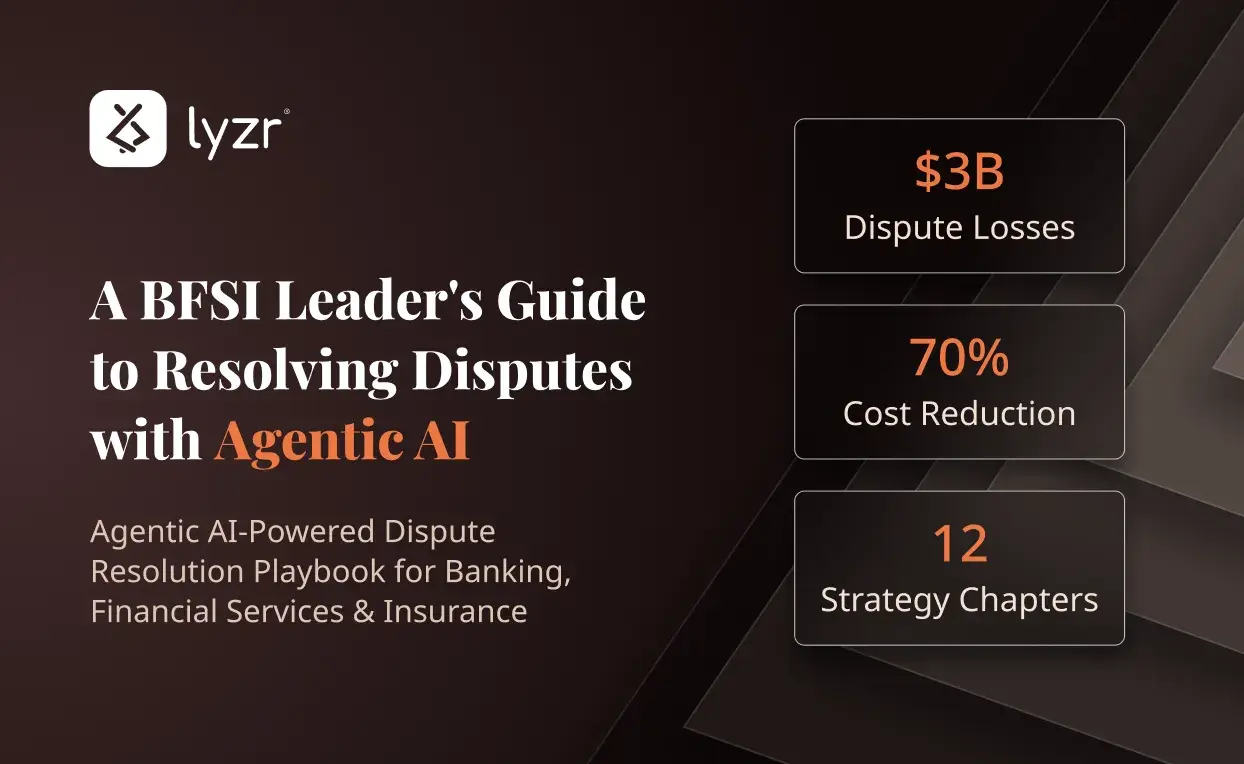

Dispute management in banking is reaching a breaking point. Between 50 million and 100 million disputes occur annually in the United States alone. The top 15 US banks collectively spend $3 billion every year processing them, and that cost is growing at 16% annually as digital payment volumes climb toward $20 trillion globally by 2033.

Traditional approaches like manual case handling, siloed systems, reactive workflows, cannot scale to meet this demand. One major bank processes 9 million disputes per year with 750 dedicated staff members. No bank can hire its way out of a 400% increase in transaction volume.

Agentic AI represents a qualitatively different solution. Unlike rule-based automation or simple AI copilots, agentic systems can perceive context, reason through ambiguity, plan multi-step actions, and execute decisions independently, while escalating to humans only when genuinely needed.

Lyzr’s AgenticOS is an enterprise-grade platform built especially for regulated industries. It provides the infrastructure banks need to deploy autonomous dispute resolution agents securely, privately, and with full governance, without replacing existing core banking systems.

Key Findings:

Agent dispute workflows significantly improve efficiency, reduce costs, and enhance customer trust, especially in the BFSI sector.

Key Insight: 62% of consumers say their trust in a financial institution is shaped more by how disputes are handled than by the original fraud incident. Dispute management is not back-office operations, it is customer relationship infrastructure. – Trust in Banking consumer research by Quavo

1. The State of Dispute Management

Understanding the scale, cost, and systemic pressures facing BFSI today

Dispute management has always been a complex, high-stakes function in banking. But the environment has shifted fundamentally. Digital payment infrastructure, real-time transaction networks, and the explosion of card-not-present commerce have created a dispute ecosystem that traditional operating models were never designed to handle.

1.1 The Volume Problem

The scale is staggering. Between 50 million and 100 million disputes occur annually in the United States alone. Last year, Americans disputed a remarkable $83 billion in charges, a figure that reflects both rising fraud and a shift in consumer expectations around dispute resolution.

Digital payments are projected to grow from $3.5 trillion to $20 trillion globally over the next eight years a roughly 400% increase. This growth will drive dispute volumes to levels that make current staffing models economically indefensible.

1.2 The Cost Problem

The financial burden is equally significant. McKinsey reports that the top 15 US institutions spend approximately $3 billion annually on chargeback management and dispute handling. Making matters worse, chargeback process costs have increased 16% compared to 2022.

At an average of $37 per dispute ranging from $10 for simple cases to $70 for complex ones the cost per interaction is substantial. For a bank processing 9 million disputes annually, that represents a direct operational cost exceeding $333 million per year before regulatory overhead, staffing burden, or customer attrition costs are factored in.

1.3 The Timeline Problem

While the industry best practice targets 30-day resolution, many financial services organizations still take up to 120 days to close complex cases. This is not merely an operational metric, it is a customer relationship issue.

Across the industry, 62% of consumers indicate that their trust in a financial institution is shaped more by the dispute experience than by the original fraud incident. Every day a case sits unresolved is a day that trust erodes. And with real-time payment adoption growing, customers now expect dispute resolution timelines to match the speed of the original transaction.

1.4 The Compliance Complexity

Beyond cost and volume, regulatory requirements are intensifying. Dispute resolution must comply with a layered set of obligations spanning card network rules (Visa, Mastercard), consumer protection regulations (Regulation E, Regulation Z, FCRA), and jurisdiction-specific frameworks across the geographies where banks operate.

Every decision must be documented. Every action must be traceable. Every policy must be applied consistently. For manual processes, this creates a permanent tension between speed and compliance and it is one that rule-based automation alone cannot resolve.

2. Why Traditional Management Fails

Six structural failure modes that make conventional dispute workflows unsustainable

Most banks have invested heavily in dispute management over the past decade. They have deployed ticketing systems, compliance workflows, partial automation, and outsourced contact center capacity. Yet costs continue to rise, timelines remain long, and customer satisfaction scores in this area consistently lag other banking touchpoints. This is not a failure of effort. It is a structural limitation of the underlying approach.

Failure Mode 1: The Search Problem

In traditional environments, agents retrieve information manually across multiple systems. A single dispute often requires accessing core banking data, card network records, CRM history, merchant information, and policy documentation from five or more disconnected platforms. Skilled agents spend 20–40 minutes per case just gathering information.

Failure Mode 2: Siloed Systems, Fragmented Experience

Dispute resolution spans systems that were never designed to operate as one: core banking, card networks, CRM, fraud monitoring, compliance databases, and communication channels. Data models differ. Real-time integration is limited. The experience feels disconnected internally and externally.

Failure Mode 3: Inconsistent Decision-Making

Policy consistency is a regulatory requirement. Yet in manual workflows, interpretation varies across agents, teams, and geographies. Two similar cases can produce different outcomes depending on who handles them, creating regulatory exposure during audits and customer inequity.

Failure Mode 4: Reactive Rather Than Preventive

Traditional dispute management begins when a customer reports a problem. There is no structured prevention layer. Yet up to 25% of disputes are predictable based on transaction behavior, merchant patterns, or customer history.

Failure Mode 5: Compliance as an Afterthought

In rule-based environments, documentation is assembled after resolution. Audit trails are reconstructed, not generated in real time. Regulatory reporting requires manual effort. Compliance becomes a parallel process instead of an embedded one.

Failure Mode 6: No Scalable Path

Traditional models tie dispute volume directly to staffing. 9 million disputes require 750 FTEs today. At projected payment growth, that model demands thousands more. This is not economically viable. Without breaking the volume-to-headcount link, dispute management remains a growing cost center.

Industry Data 88% of financial services leaders agree that organizations need to innovate faster. But 75% struggle to implement new payment solutions due to outdated infrastructure. – Forrester study commissioned by AWS Marketplace, 2025

3. Understanding Dispute Types

A taxonomy of dispute categories, complexity tiers, and routing logic

Not all disputes are equal. A robust agentic dispute management system must distinguish between dispute types that require fundamentally different resolution paths, evidence requirements, and regulatory handling. The first step in any implementation is building a comprehensive taxonomy of dispute categories specific to your institution.

3.1 Fraud-Related Disputes

Fraud disputes involve unauthorized use of customer payment credentials or accounts. They carry the highest regulatory urgency, the strongest consumer protection obligations, and the most significant fraud liability risk for the institution.

3.2 Non-Fraud / Service Disputes

Service disputes involve legitimate transactions where something went wrong, a billing error, a service failure, or a dispute with a merchant. These require different evidence standards and resolution pathways than fraud cases.

- Duplicate or erroneous charges: same transaction processed twice, or incorrect amount billed

- Goods or services not received: customer paid but delivery failed or service was not rendered

- Billing and currency errors: incorrect currency conversion, subscription billing errors, fee disputes

- Merchant chargeback representment:bank disputes a chargeback on behalf of a merchant

- Real-time payment disputes: growing category as instant payments eliminate traditional recall windows

- ATM and branch transaction errors: physical transaction discrepancies requiring reconciliation

3.3 Complexity Tiers

Beyond category, disputes should be classified by complexity to determine appropriate levels of AI autonomy and human oversight.

4. The Automation Maturity Model

Four stages from manual to agentic and where your institution sits today

Understanding where your institution sits in the automation maturity model is the essential first step before designing any AI implementation. Most BFSI institutions are not starting from zero; they have some level of automation in place. The question is what tier they are at, and what it will take to advance.

Stage 1: Fully Manual

Characteristics: Every case handled from scratch by human agents. No automated routing, no AI-assisted evidence gathering, no policy enforcement automation. Systems are largely siloed, requiring agents to navigate 5+ platforms per case.

Typical metrics: 30-40 minute average case handling time, 30-120 day resolution cycles, 35 FTEs per 1M disputes. Compliance is agent-dependent, audit preparation is reactive, and outcomes vary significantly by case handler.

Stage 2: RPA-Augmented

Characteristics: Robotic Process Automation handles repetitive tasks: data entry, status notifications, form routing, basic report generation. Humans remain central to all decision-making. RPA follows fixed scripts and cannot handle exceptions.

Typical metrics: 15–20% effort savings on routine tasks. Handle time reduced slightly (25–30 minutes). But RPA creates its own fragility, when system interfaces change, bots break. Technical debt accumulates.

Stage 3: RPA + Intelligent Document Processing + Human-in-the-Loop

Characteristics: AI handles document extraction and validation (IDP), enabling automated processing of PDFs, statements, and supporting documents. Human-in-the-loop (HITL) oversight applies to edge cases and decisions above defined confidence thresholds.

Typical metrics: 40–50% effort savings, first-time-right accuracy exceeds 75% for document-heavy cases, compliance documentation significantly improved. This is where many leading BFSI institutions sit today.

Stage 4: Agentic Automation

Characteristics: Autonomous agents independently reason through cases, retrieve evidence, apply policy, determine resolutions, and communicate outcomes. Humans are involved only by exception, on complex cases, high-stakes decisions, and regulatory escalations. The system learns from outcomes and continuously improves.

Typical metrics: 80-90% of disputes fully resolved autonomously. Average resolution time reduced to minutes for Tier 1 cases. Cost per dispute falls below $12 for AI-handled cases. 90%+ first-time-right accuracy. Full audit trail generated automatically.

5. What is Agentic AI in Dispute Management?

The term ‘AI in banking‘ has been used to describe everything from simple chatbots to sophisticated fraud detection models. Agentic AI represents a genuinely distinct capability, and understanding that distinction is essential for setting realistic expectations, designing appropriate governance, and communicating the change to stakeholders.

5.1 The Definition

Agentic AI refers to autonomous systems that can perceive context, reason through complex scenarios, plan multi-step actions, and execute decisions independently over extended timeframes. In dispute management, this means:

- An agent that doesn’t just route a case, it reads the transaction data, retrieves merchant history, checks the customer’s behavioral profile, applies the relevant card network rules, and determines the appropriate resolution all without being explicitly programmed for that specific scenario.

- An agent that can handle variability and ambiguity, not just the predictable, rule-following patterns that RPA was designed for.

- An agent that learns from outcomes, updating its confidence thresholds and resolution patterns based on what worked and what didn’t.

5.2 How Agentic AI Differs from Prior Approaches

5.3 Core Agentic Capabilities in Dispute Resolution

Market Context: McKinsey’s research indicates that 85% of institutions already deploy some form of AI. But the gap between ‘AI in the building’ and ‘AI reliably resolving disputes at scale’ is precisely the gap that agentic architecture closes.

6. The Dispute Resolution Lifecycle

Stage-by-stage breakdown of the agentic dispute workflow

A complete agentic dispute resolution workflow spans six distinct lifecycle stages. Each stage has specific data requirements, decision logic, agent responsibilities, and human oversight checkpoints. Understanding this lifecycle in detail is essential for designing the right agent architecture and governance model for your institution.

Stage 1: Intake & Multi-Channel Unification

Disputes arrive through multiple channels: phone calls, mobile app submissions, web portal forms, branch visits, and increasingly, proactive agent-initiated alerts. Traditional systems handle each channel separately, creating duplicate case files, missed context, and inconsistent handling.

In an agentic system, the Dispute Resolution Agent consolidates all incoming disputes into unified case files regardless of entry point. A customer who files via the app and then calls to follow up is recognized as the same case, with the full interaction history available to every agent touchpoint. Duplicate cases are automatically detected and merged.

- Primary agent: Dispute Resolution Agent

- Key action: Multi-channel intake consolidation, initial fraud vs. non-fraud triage

- Human checkpoint: None required for standard cases

- Outcome: Unified case file created, initial classification assigned, routing decision made

Stage 2: Evidence Gathering & Investigation

This is where agentic AI delivers its most dramatic efficiency gain. Human agents spend 60–70% of their case handling time gathering evidence: accessing core banking records, card network data, merchant details, and supporting documentation.

The Transaction Monitoring Agent retrieves all relevant data autonomously within seconds of case creation. This includes the full transaction record, the cardholder’s spending profile and behavioral history, merchant dispute frequency data, any prior interactions with the same merchant, and all relevant payment network records.

- Primary agent: Transaction Monitoring Agent

- Key action: Autonomous retrieval of transaction data, merchant records, cardholder history

- Human checkpoint: None required, all evidence is surfaced and structured

- Outcome: Complete evidence package compiled, confidence score assigned

Stage 3: Fraud Detection & Risk Scoring

With evidence compiled, the Fraud Detection Agent and Risk Scoring Agent work in parallel to assess the legitimacy of the dispute claim and assign a dynamic risk score to guide resolution routing.

For unauthorized transaction claims, agents analyze behavioral patterns to verify whether transactions align with established spending profiles. For friendly fraud detection, where customers dispute legitimate transactions, agents identify the behavioral and contextual markers that distinguish genuine disputes from first-party fraud attempts. A confidence score is assigned to every classification decision, and cases below the confidence threshold are flagged for human review before resolution proceeds.

- Primary agents: Fraud Detection Agent, Risk Scoring Agent

- Key action: Pattern analysis, behavioral profiling, confidence scoring

- Human checkpoint: Cases below 0.95 confidence threshold escalate automatically

- Outcome: Risk classification, confidence score, resolution path determined

Stage 4: Resolution & Decision

The Policy Enforcement Agent applies the institution’s dispute resolution policies to the assembled evidence and risk assessment. For Tier 1 and Tier 2 cases where confidence is high and policy is clear, the agent determines the resolution autonomously. For Tier 3 and Tier 4 cases, the agent prepares a complete case brief, including the evidence package, risk score, and policy recommendation, for human review.

This is the stage where the kill switch and human override protocol matters most. The system must have defined thresholds for when AI acts alone and when human judgment is required. These thresholds should reflect transaction value, regulatory sensitivity, dispute complexity, and institutional risk appetite.

- Primary agent: Policy Enforcement Agent, Explainability Agent

- Key action: Policy application, decision documentation, escalation where required

- Human checkpoint: Mandatory for Tier 3/4, high-value, and regulatory-sensitive cases

- Outcome: Resolution decision made, documentation generated

Stage 5: Provisional Credit & Settlement

For cases where the resolution favors the customer, the Settlement Processing Agent manages provisional credit issuance and final settlement cycles. Provisional credits are issued automatically for qualifying cases, reducing the 30-120 day wait that damages customer relationships, while the investigation continues.

For chargeback representment (defending valid merchant transactions against illegitimate disputes), the agent automatically compiles the evidence package and submits to the appropriate card network within the required timeframe.

- Primary agent: Settlement Processing Agent

- Key action: Provisional credit issuance, settlement cycle management, chargeback filing

- Human checkpoint: Required for high-value provisional credits above defined thresholds

- Outcome: Customer credited, settlement recorded, chargeback filed where applicable

Stage 6: Audit Documentation & Compliance Reporting

Every action taken by every agent at every stage is logged in real time to an immutable audit trail. The Regulatory Reporting Agent and Audit Preparation Agent ensure that all required documentation is generated continuously, not assembled reactively when a regulator asks.

This means that when an audit occurs, the complete case history, every data access, every decision, every confidence score, every escalation trigger, is available for immediate review. The decision ‘thought process’ can be replayed. Compliance reports are generated automatically on the required schedule.

- Primary agents: Regulatory Reporting Agent, Audit Preparation Agent

- Key action: Immutable trail creation, automated regulatory report generation

- Human checkpoint: Final sign-off on regulatory submissions

- Outcome: Full audit package, compliance reports, regulatory-ready documentation

7. Lyzr Agent Architecture Deep Dive

The specific agents, their functions, and how they orchestrate

Lyzr’s AgenticOS provides a pre-built set of banking-specific agents that can be deployed individually or as an orchestrated suite. Each agent comes pre-configured with dispute-specific guardrails, policy templates, and integration patterns. This chapter describes each agent’s function, configuration requirements, and integration dependencies.

The Lyzr AgenticOS

All dispute agents operate through Lyzr’s Agentic OS, the platform layer built on Agent Studio that provides governance controls, reasoning infrastructure, audit logging, LLM abstraction, and multi-agent orchestration. This is what makes individual agents governable, auditable, and interoperable without replacing existing core banking infrastructure.

Core Dispute Agents

Using Lyzr’s Agent Studio, institutions configure purpose-built agents for each stage of the dispute lifecycle. These agents are composable, deployed individually or as an orchestrated suite, and come with pre-built blueprints for common banking workflows.

The table below describes the functional agent types typically deployed in a dispute resolution implementation.

Integration Architecture

Lyzr’s AgenticOS acts as the intelligent middleware fabric between your systems of record and systems of action. It reads from existing infrastructure, reasons with secure LLMs, and writes refined decisions back, without requiring replacement of core systems.

8. Zero-Trust Governance Framework

The non-negotiable governance model for agentic AI in regulated environments

Governance is not an add-on to agentic AI in BFSI, it is the foundation. The institutions that fail at AI governance fail visibly: regulatory actions, customer harm events, security breaches, and expensive rollbacks. The institutions that get it right deploy with confidence and scale without incident.

Lyzr’s platform is built governance-first. Every capability described in earlier chapters operates within a zero-trust governance model where no agent is trusted by default, all actions are verified and logged, and human override is always available.

8.1 The Permission Layer (RBAC)

Role-Based Access Control in Lyzr’s system operates at the agent level, not just the user level. Every agent has a defined permission set that specifies:

- Which APIs the agent can call (and with what parameters)

- Which data subsets the agent can read (customer data, transaction records, third-party feeds)

- Which systems the agent can write to (core banking, CRM, card networks)

- Which actions require human authorization before execution

- Which actions can never be executed autonomously regardless of confidence

RBAC permissions are defined and enforced by the AgenticOS; they cannot be overridden by individual agent logic. This architecture ensures that even if an agent encounters unexpected input or operates outside its training distribution, it cannot exceed its defined authority boundary.

8.2 Tiered Autonomy Model

Rather than a binary ‘AI acts alone or AI doesn’t act,’ Lyzr implements a tiered autonomy model that matches agent authority to case risk and complexity:

8.3 The Kill Switch & Human Override

Every agent in the Lyzr platform can be suspended instantaneously by authorized personnel. The kill switch operates at three levels:

- Individual case level: suspend agent action on a specific dispute while investigation continues

- Agent level: suspend a specific agent (e.g., the Settlement Processing Agent) without affecting others

- System level: suspend all autonomous agent activity while maintaining case records and audit trails

Human override checkpoints are hardcoded into the workflow for defined scenarios, they cannot be disabled by configuration. Any case involving transaction values above the defined threshold, regulatory flags, litigation history, or VIP customer designations requires mandatory human sign-off before resolution completes.

8.4 Immutable Audit Trail & Decision Replay

Every agent action, every API call, every data access, every confidence score, every escalation trigger, every decision, is logged to an immutable ledger in real time. This is not a traditional application log. It is a structured, searchable, replay-capable record of the agent’s complete ‘thought process’ for every case.

Specifically, the audit trail records:

- What data was accessed, from which system, at what time

- What the agent’s intermediate reasoning steps were

- What confidence score was assigned and why

- Which policy rule was applied and the basis for that selection

- What escalation was triggered and to whom

- What the final resolution was and the complete evidence that supported it

This replay capability is transformative for regulatory interactions. When a regulator requests an explanation of a specific dispute resolution, the complete decision history can be provided and re-executed for their review.

8.5 Compliance & Certification

Lyzr’s platform holds the following certifications relevant to BFSI deployment:

- SOC 2: Security, availability, and confidentiality controls

- ISO 27001: Information security management system certification

- GDPR Ready: Data privacy architecture for EU/UK deployment

- HIPAA Compliant: Healthcare and financial data handling standards

- CCPA Compliant: California Consumer Privacy Act data standards

Accenture on Lyzr: Lyzr’s platform lets companies create secure, explainable and compliant AI agents that can automate decisions across workflows, helping to modernize slow manual processes and enhance operational efficiency. Its responsible AI features enable agents to drive value while effectively navigating the complexities of heavily regulated industries.

— Kenneth Saldanha, Global Lead, Accenture Insurance Industry Practice

9. Human-AI Collaboration Model

When AI acts alone, when humans step in, and how to design the handoff

The most successful dispute management implementations are not those that maximize AI autonomy, they are those that deploy AI and human judgment where each is most effective. Getting this balance right requires explicit design, not an afterthought.

Genpact estimates a 50% reduction in operational time spent on case reviews when AI handles routine cases autonomously. Human agents then focus their expertise on the 20% of cases that genuinely require nuanced judgment. This is not automation threatening jobs, it is automation enabling analysts to do analytical work.

9.1 The Collaboration Matrix

9.2 Designing the Escalation Protocol

The escalation protocol defines the conditions under which an agent transfers a case to a human and critically, how that transfer happens. A poorly designed handoff is nearly as damaging as no human oversight at all.

Effective escalation protocols define:

9.3 The Handoff Package

When Lyzr’s Agent prepares a case for human review, it generates a structured handoff package that ensures the human agent can make a decision without needing to reconstruct the investigation from scratch. This package includes:

- Transaction details: full record of the disputed transaction(s) with metadata

- Customer profile summary: relevant account history, dispute history, risk profile

- Evidence inventory: all documents and data retrieved, with source references

- AI reasoning summary: what the agent determined and why, in plain language

- Confidence score and rationale: why the threshold was not met

- Policy references: the specific rules applicable to this case

- Recommended action: the agent’s best-judgment resolution, for human consideration

- Sentiment signals: indicators of customer distress level from communication analysis

Human agents don’t restart: they review a complete brief and apply their judgment to the specific dimension that requires it. This dramatically reduces the average handle time even for escalated cases.

Customer Trust 74% of consumers say that transparency in fraud investigations builds trust. When human agents are visibly involved in appropriate cases, customers feel their concerns receive genuine attention, even if an AI handled the investigation.

10. Implementation Roadmap

A practical 4-week deployment path with longer-term scaling milestones

Lyzr’s implementation approach is deliberately rapid. Most BFSI organizations are not starting from zero, they have existing systems, data infrastructure, and automation investments. The 4-week deployment path is designed to build on this foundation, not replace it.

The fundamental principle: start with a bounded, low-risk use case, demonstrate measurable results, then expand. This builds organizational confidence, demonstrates ROI to leadership, and identifies integration edge cases before they affect the full dispute portfolio.

Scaling Roadmap: Months 2-12

11. Dispute Intelligence Scorecard

Use this scorecard with your operations, technology, and compliance leadership to benchmark your current dispute management capability against agentic Al targets. Score each KPI honestly based on today’s state, not aspirations. The total score reveals where you sit on the Dispute Intelligence Maturity scale and where to prioritize.

Complete this as a team exercise. Disagreement between scores across departments is itself a diagnostic signal, it indicates inconsistency in how the function is measured or understood.

11.1 Operational Efficiency KPIs

11.2 Customer Experience KPIs

11.3 Financial ROI KPIs

11.4 Compliance & Governance KPIs

Your Dispute Intelligence Score

Add up your section totals below to calculate your overall Dispute Intelligence Score out of 92, then find your maturity band on the scale below.

Score Interpretation

Turning Your Score into Action

Once you have your total score, identify the two or three KPIs where your score is lowest, these are your highest-leverage improvement opportunities. Use the framework below to prioritize:

11. 5 Modeled Financial Impact Scenarios

12.Getting Started

Your readiness assessment, first steps, and how to engage

Transforming dispute management from a cost center into a competitive differentiator is achievable within a realistic timeframe. The institutions that move with deliberate urgency, building on existing infrastructure, establishing governance frameworks before deployment, and starting with bounded pilots, see measurable results within weeks.

12.1 Readiness Self-Assessment

Before getting started, conduct this rapid readiness assessment across five dimensions. Score each on a 1–4 scale (1 = Stage 1, 4 = Stage 4 from Chapter 4’s maturity model).

Dispute Management Readiness Checklist

Use this checklist before beginning your agentic dispute management implementation. Items marked as critical must be completed before go-live.

Next Steps

Book a Strategy & Demo Session

If you’re evaluating agentic dispute management for your organisation, schedule a 15-min call.

We’ll:

- Map your dispute workflow against the maturity model

- Identify your highest-leverage pilot category

- Define deployment scope and governance design

- Outline a 4–6 week path to production

Explore Banking Agents

See how Lyzr’s banking agents operate across:

- Dispute resolution

- KYC and compliance

- Fraud workflows

- Risk scoring

- Regulatory reporting

Designed for secure VPC deployment and full auditability. Explore Banking Agents.